As Industry 4.0 continues to be a point of focus for forward-thinking companies, one question we keep hearing is what impact will blockchain have on the food industry.

It is a good question as, on paper, the idea of utilising blockchain technology helps solve many problems the industry faces. But will there really be an impact or is it just the hot new thing right now with no realistic chance of being adopted?

Let’s look at what blockchain is and what impact it will have on the food industry in the future.

What is blockchain?

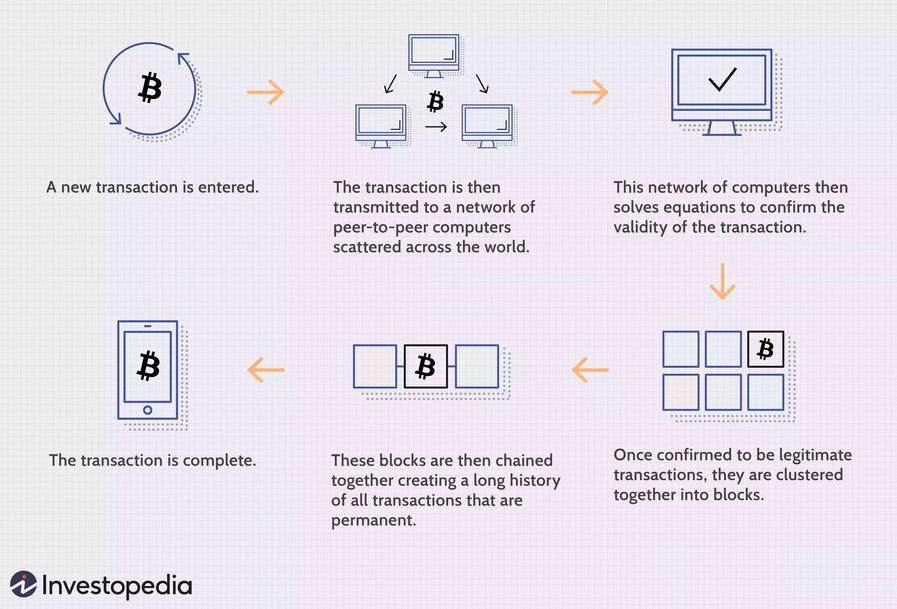

To boil it down to the simplest form, a blockchain is a type of database or ledger that is used to keep track of and record data. Information is collected in groups, known as blocks, with each block holding a set of information that is chained to previous blocks once full. Rather than this information being held in one place, it is a distributed ledger, meaning there are multiple copies that are used to verify information is correct.

This might sound complicated, but the important parts are the distributed nature of information that is linked, forming an irreversible timeline of data.

What does this mean for the food industry?

While there has still been little adoption, the leading companies in the food industry are looking at how they can implement blockchain into their operations. Due to the irreversible timeline of a blockchain, there is real value in utilising it throughout the supply chain.

Food safety is a key issue within the industry, with recalls being costly and damaging to the reputation of companies. Blockchain can help here by recording transaction records as a product moves through the supply chain. Take a piece of meat as an example, it must go from a farm to producers, distributors, and sellers, before reaching consumers which results in many different contact points.

A blockchain can have a full record of everything that meat has been through, from the farmer it started at, shipping information, and even what temperature it was stored at! This timeline of information is vital in ensuring product safety or working out where issues have occurred when they arise.

Other impacts blockchain will have on the food industry

Longer term, the biggest impact blockchain will have on the food industry is the increased trust and loyalty of consumers. Giving consumers the ability to see a full timeline of where their product has been along with the conditions will boost their confidence in the brands they buy from. They will have a level of transparency that has never been possible and the error-free nature of blockchain will only add to that confidence.

Another major area will be the adoption and utilisation of smart contracts within the food industry. Smart contracts are programs stored on a blockchain that are set to run when predetermined conditions are met. For example, once a retailer receives a shipment of stock, the pre-agreed payment is released to the supplier. The benefit of these smart contracts is once they are agreed they cannot be changed, giving trust and transparency to any deal. They also represent an unrivalled level of speed, efficiency, and accuracy that is not possible with traditional systems.

The final impact that blockchain will have on the food industry is an increase in security across companies that adopt it. Blockchain transaction records are encrypted and chained with each record that came before and after, meaning any bad actors would need to hack the entire chain to change a single record.

Conclusion to what impact will blockchain have on the food industry

As the food industry continues to adopt Industry 4.0, the benefits of utilising blockchain technology will become more and more appealing. Companies in the food industry that adopt blockchain will have unrivalled security and transparency over their supply chain, which can be used to monitor products as they move towards the end consumer. Long term, these changes will build consumer confidence in the products they buy and encourage them to buy more from companies who have the best practices in place.